22 June 2025

The breaking news this morning that the US has carried out attacks on Iranian nuclear facilities marks a potentially serious escalation in the Middle East. That the US has joined Israel in its strikes against Iran undermines optimism that the conflict between Israel and Iran, which began on 13 June, could be de-escalated quickly.

What has happened?

- The US has bombed three Iranian nuclear sites: Fordow, Natanz, and Isfahan. According to The New York Times, six B-2 bombers dropped bunker-buster bombs on Fordow, while submarines fired cruise missiles at Natanz and Isfahan. The International Atomic Energy Agency has reported no increase in radiation detected around the sites hit.

- US President Donald Trump has said in a national address that the “US military carried out massive precision strikes… to destroy Iran’s nuclear enrichment capacity.” Signalling an openness to talks, Trump said that Iran must now “make peace” or face further, “greater” attacks.

- Various media reports suggest that Iran is considering how to respond. Its Foreign Minister, Abbas Araghchi, warned of “everlasting consequences” to these “outrageous” US strikes.

As the situation is in flux, and a host of potential scenarios are now live possibilities, we can only speculate about exactly what happens next and what the economic consequences may be. Here are my 10 initial observations:

- Possible Iranian response: A lot now depends upon how Iran reacts. While it is not inconceivable that Iran responds to US attacks via diplomatic channels, that seems unlikely based on the initial verbal response of its foreign minister and past experience. In case of retaliation, the next possible steps could include the following:

- First, Iran may launch attacks on US bases with sufficient prior warning – i.e. an attack that makes a face-saving statement but does not necessarily invite a hot response by the US. We saw something similar in January 2020 during Trump’s first term, when Iran responded to the assassination of Major General Qasem Soleimani. Such a response could precede a de-escalation or even the re-starting of negotiations over Iran’s nuclear programme.

- Second, Iran could launch surprise direct attacks on US bases or sites housing its military personnel – intending to inflict damage that the US could not easily overlook without retaliating.

- Third, there could be retaliatory attacks by Iranian proxies – including Hezbollah and the Houthis. This could occur independently or alongside the first and second points outlined above.

- Or fourth, in a worst-case scenario, Iran might attempt to strike or mine the Strait of Hormuz or attack neighbouring oil and gas facilities to try to inflict economic damage on the US. However, as noted in point 7 below, this would risk far-reaching collateral damage, including potentially to Chinese economic interests. This represents a tail-risk scenario, in our view.

- US-Israeli objectives: Of the four possible scenarios set out above, de-escalation and diplomacy would be the one which quickly reduces risks to the global economy associated with an escalatory spiral, while the fourth ‘tail-risk’ outcome involving a global supply shock would be the most severe. However, given that this was co-ordinated and planned jointly by the US and Israel, much now depends on the joint objectives of Washington and Tel Aviv. We can only offer two questions at present:

- Do the US and Israel desire a complete end to Iran’s nuclear programme—either via total destruction or agreement (and on what terms)? It may take days to confirm the actual damage inflicted on Iranian sites.

- Or, as has been hinted at previously by Israeli Prime Minister Benjamin Netanyahu, are the US and Israel seeking regime change in Iran? The danger in this scenario is that Iran may opt for an all-or-nothing response, which could involve targeting the Strait of Hormuz as well as regional oil facilities, including those in Saudi Arabia.

- Difficulties in restarting nuclear talks: In speculating about hope for a diplomatic resolution that limits Iran’s nuclear programme, the challenge for the US and Israel will be ensuring that Iran holds up its end of any agreement. If Tehran perceives that its regime is under existential threat—and the falls of other Middle Eastern regimes in Iraq, Libya, and Syria in recent years suggest this should be a worry—the danger is that Tehran will simply try to buy time in order to accelerate the development of an operational nuclear weapon.

- Keeping the conflict contained: Even though US involvement represents a widening of the conflict, at present, the US and Israel appear to be in control and the risk of a domino effect around the Middle East seems low. From a distance, Iran and its proxies appear badly weakened, and Israel has air superiority over Iran – including widespread reports that it controls Tehran airspace. For the US and Israel, the objective may be—having demonstrated remarkable intelligence capabilities and an ability to destroy Iranian targets at will—to seek a total resolution of the risks posed by the Iranian regime, its push for nuclear armament, and sponsorship of terrorism.

- Guessing the market reaction: Predicting how markets will react in such circumstances is difficult. Having read the breaking news early this morning, I had anticipated a negative reaction in Israeli and Saudi Arabian stock markets – which are open on Sunday – as part of a knee-jerk risk-off move. However, those markets are up today—perhaps reflecting hopes that Iran’s nuclear facilities have been so badly damaged that its weapons programme has been stopped, thereby reducing the overall threat that Iran poses to the region and the world and removing a host of longer-run tail risks.

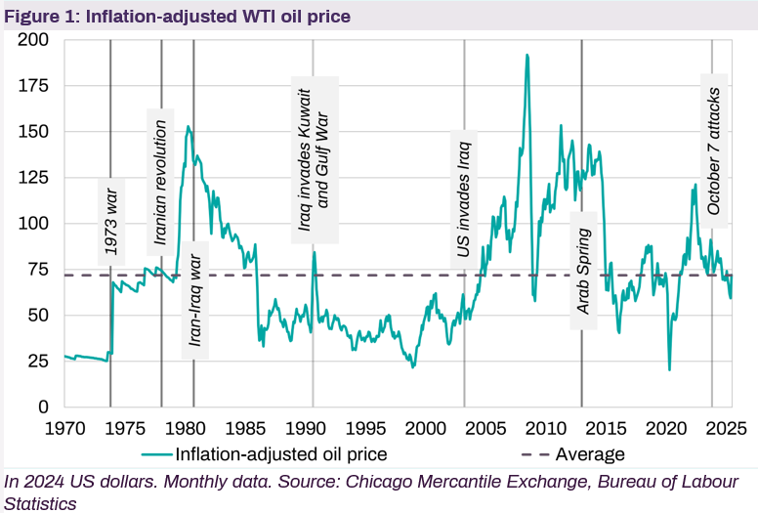

- Key few days ahead: As the situation is developing, and for now we have many more questions than answers, the initial market reaction may not provide a useful guide to what could unfold over coming days and weeks. In all likelihood, we will be able to judge, based on any follow-up from either side, what the most likely scenario will look like. Critically, while the risk of another global energy supply shock now looms large, it remains a tail-risk scenario, not a base case. Aside from the OPEC shocks in the 1970s, past escalations in the Middle East suggest that disruptions to energy markets tend to resolve quickly (Figure 1).

- Risks to energy supplies: When assessing the potential risks to the global economy, the immediate worry comes from disruptions to global oil and gas supplies. On the one hand, because Iranian oil and gas exports account for less than 2% of the global total, disruptions to its ability to produce and export hydrocarbons would be serious for the world but manageable – as any drop-off could be partly or fully offset by increased production elsewhere. On the other hand, however, more than a fifth of global oil and gas flows through the Strait of Hormuz—which is on Iran’s southern coast and just 21 miles wide at its narrowest point—and thus could be a viable target for Iran. An attempt by Iran to attack or mine the Strait would represent a much more severe economic risk scenario, causing a significant global supply and price shock, depressing global GDP and pushing up inflation. That said, it is worth noting that China is heavily dependent on the Strait of Hormuz for its trade. If Iran tries to block that stretch of water, it risks an all-out war with the most powerful country in the world (the US) and badly antagonising the second most powerful (China).

- Economic impact probably limited: Although the risks have increased appreciably, the economic impact of the escalation is likely to be limited unless the worst-case scenario unfolds. That assumption should hold as long as it remains clear that Israel and the US have the upper hand and while ever global oil and gas flows are not disrupted in a major way (this will likely be the market’s working assumption unless evidence emerges to the contrary). In the near term, with two-way risks depending on developments, it is possible that markets may struggle for direction—leading to gyrations but no major net shifts. Until further major developments, expect oil and gas prices to rise, while currencies and bonds remain mostly stable. The direction of the dollar may indicate whether recent worries about the global reserve currency losing safe haven status are justified. Headlines predicting oil prices above $100 a barrel should be viewed as forecasts for worst-case scenarios at this stage. If Middle Eastern equity markets remain green at the end of trading today, and Iran does not retaliate against the US overnight, European and US markets may even be flat or slightly up tomorrow. For better or worse, risk appetites have proven resilient in recent months.

- Trump is a wildcard: We should also keep in mind that Trump is an unconventional president. Only days ago, he hinted that the US would decide in the next two weeks whether to strike Iran, suggesting a possible timeline and deadline for talks. But that proved to be a feint. This adds to uncertainty, making any past experience of how the US may conduct itself and how this situation may unfold a less useful guide. Critically, it is not yet clear what the US's endgame is.

- Central banks in a bind: Adding to the risks, central banks would have a difficult time easing monetary policy aggressively in a downside scenario in which global oil and gas supplies are badly disrupted and inflation spikes. After the 2022–23 inflation surge, which too resulted from a global energy shock, price expectations are not sufficiently well anchored in advanced economies—most notably in the US following Washington’s erratic tariff policies—for central banks to look through any renewed inflation shock and pre-emptively lean against economic weakness. In the US, we look for two more 25bp cuts this year to take the Funds Rate upper limit to 4.0% by year-end – followed by another 50bp of cuts next year. In the UK, we expect the BoE to reduce the Bank Rate from 4.25% to 3.75% by end-2025. In the Eurozone, we project that the ECB will cut the deposit rate from 2.00% to 1.75% by end-2025, before the bank raises rates again by 50bp in 2026. The heightened risk of a bout of energy price inflation tilts the risks to our calls towards fewer cuts.