QUICKTAKE

- The UK’s policymaking credibility is damaged, and the government needs a new mechanism to signal fiscal discipline to markets. Elevated interest rates reflect genuine worries about the UK’s commitment to sound money.

- High household saving and soft consumption since 2022 coincide with a major shock to household net wealth. Persistently high interest rates, reflecting policy worries, hold back asset prices and come at a bad time.

- Benchmark interest rates are above levels needed to produce a healthy cyclical upswing in the private sector – soft UK momentum looks like a classic case of crowding out.

Sound money matters

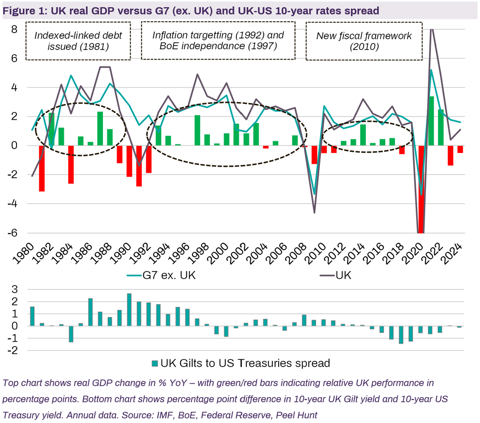

What do index-linked debt, Bank of England (BoE) independence and the Office for Budget Responsibility (OBR) have in common? Each was, at critical moments, a successful and necessary advance in the UK’s economic policy framework. These reforms restored policymaker credibility following periods of economic malaise, or policy mistakes.

Since the early 1980s, the UK has experienced repeated cycles of improvement and setbacks to policymaker credibility, corresponding with periods of relative economic success compared to other advanced economies (Figure 1).

This historical pattern helps explain the UK’s current lacklustre growth, subdued confidence, elevated bond yields, and cyclical weakness after a succession of shocks and policy mistakes.

It also suggests that Labour’s fundamental policy challenge goes well beyond balancing the books at the 26 November Budget. To offset the decline in British policymaking credibility — which began before Labour took office — requires fresh thinking and a new approach that delivers a credible commitment to sound public finances and price stability.

Cycles of credibility: a historical perspective

After winning the 1979 election, Margaret Thatcher’s Conservative government sought to restore sound money after a series of inflationary crises in the 1970s. As part of a broad programme of austerity and deregulation, the Thatcher government began issuing index-linked debt in 1981, protecting lenders against inflation by guaranteeing a real rate of return. From 1982 to 1988, the UK outpaced the G7 (excluding the UK) in every year but one.

The late 1980s brought economic trouble as expansion gave way to recession. In response, the Conservatives introduced two changes to monetary policy. First, the UK joined the European Exchange Rate Mechanism (ERM) in 1990, designed to stabilise exchange rates among European currencies, but exited in September 1992 after a painful sterling crisis. Second, in October 1992, the government introduced an inflation target for the first time, set at a 1–4% annual change in the retail price index excluding mortgage payments.

When Labour’s 1997 election victory ended 18 years of Conservative government. Chancellor Gordon Brown introduced fiscal rules in the UK for the first time — including a ‘golden rule’ that current spending and taxation should balance over the cycle, and that public debt should remain below 40% of GDP. He also granted the BoE operational independence to set policy in pursuit of a government-defined price stability target, now 2% inflation based on the consumer price index.

The post-1992 Conservative and Labour policy innovations worked. From 1993 to 2007, the UK outpaced the rest of the G7 in all but two years. But the success unravelled during the 2008 global financial crisis (GFC), when the UK suffered an outsized recession - exposing prior excesses in credit and the mortgage market, as well as a badly managed fiscal policy. The downturn and surge in public debt set back UK policymaking credibility once again.

After the 2010 election, in the wake of the financial crisis, Chancellor George Osborne of the newly-elected Conservative–Liberal Democrat coalition repeated the familiar playbook to restore credibility. Alongside a significant budget tightening and stricter fiscal rules, Osborne introduced the Fiscal Responsibility Act, mandating year-on-year reductions in public sector net borrowing from 2011 to 2016. He also established the Office for Budget Responsibility, transferring oversight of fiscal rules to an independent body and increasing transparency. Once again, the corrective measures worked: from 2012 to 2017, the UK outpaced the G7 in every year, while Gilt spreads over Treasuries narrowed.

Recent shocks and policy missteps

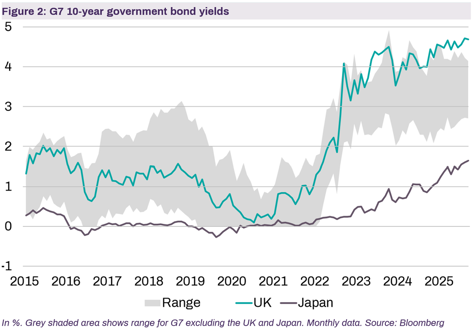

Over the past decade, a succession of shocks and policy missteps have undermined the post-GFC progress. These include the protracted and mismanaged Brexit process, the post-COVID-19 inflation surge, the September 2022 Liz Truss bond market crisis, and, more recently, a resurgence of inflation triggered by Labour’s energy, tax, and labour market policies. The result has been economic underperformance and, crucially, a sharp rise in UK benchmark rates.

As Figure 2 shows, until the September 2022 crisis, UK 10-year yields were broadly in line with G7 peers. Since late 2022, UK yields have jumped above the G7 range and remain elevated.

Under the previous Conservative government, the UK's fiscal framework was based upon two core rules: (1) the current budget rule, requiring day-to-day spending to be funded by taxes without borrowing within five years; and (2) the debt rule, mandating public sector net debt (excluding the BoE) to fall as a share of GDP within five years.

In summer 2024, Labour won a landslide election – ending 14 years of Conservative rule. But Chancellor Rachel Reeves, unlike her successful predecessors, did not take the opportunity to reconfigure or innovate the UK’s policy framework to renew a commitment to sound money. Instead, she made small modifications to the old framework – keeping the balanced current budget rule, initially with a target of 2029/30 (but with a three-year target from 2026/27 onwards) and replacing the debt rule with one that focuses on public sector net financial liabilities, initially with a target of 2029/30 (but also with a three-year target from 2026/27 onwards).

Judging by Labour’s first year in power – rising inflation, sluggish growth, and skittish bond markets – Reeves’s fiddling at the edges appears to have amplified rather than mitigated worries about UK policy credibility.

Elevated interest rates compound the 2022 wealth shock

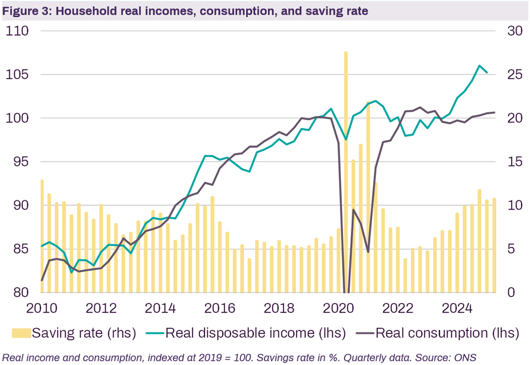

Despite elevated inflation, real household disposable income has grown solidly since 2022, in line with the 2010-19 average of 1.8% annualised. However, unlike during the post-GFC recovery, household saving has risen sharply (see Figure 3).

One argument for households’ high rate of saving is that, facing a highly uncertain economic outlook, and lingering skittishness after a decade of big shocks, the inclination to save on a precautionary basis is higher than normal. While there may be a kernel of truth to this, the story does not apply in other comparable countries — notably the US — where uncertainty is similarly high, and yet consumers saved just 4.7% of their disposable income in the first half of the year, compared to 10.6% in the UK.

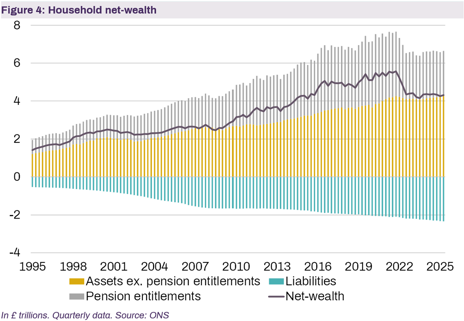

A bigger factor behind the trend of elevated saving appears to be the huge wealth shock that households suffered in 2022 (see Figure 4). From a peak of £5.6tn in 4Q21, net wealth declined to the £4.2-4.4tn range where it has hovered for almost three years. This contrasts with the steady rise in net wealth following the GFC. The ONS estimates suggest the recent slump was mostly driven by a £1tn fall in pension entitlements.

Pensions account for 35% of household net wealth, second only to housing. Pension wealth fell sharply during the 2022 correction in global bond prices (when bond prices fall, interest rates rise). The UK suffered particularly severe losses, especially during the Truss episode, which triggered a crisis in the liability-driven investment (LDI) pensions market.

Given the well-known problems with UK data, precise estimates for UK household net wealth should be taken with a pinch of salt. But even if the data exaggerate the extent of the shock, other arguments support the broader point that households’ proclivity for high saving is consistent with a wealth shock. The recent story contrasts, for example, with the robust post-Lehman expansion in household spending – which occurred alongside rapid house price growth, rising equity markets at home, and rising bond valuations as benchmark interest rates declined. Further, recent low rates of saving in the US have coincided with a c.50% increase in household net wealth since 2022 — helped by the impressive stock market rally.

Excessively high UK bond yields obstruct a recovery in household net wealth by slowing the recovery in pension assets, holding back housing market momentum, and weighing on UK equity valuations. Separately, we also see the wealth shock playing out in consumer confidence trends.

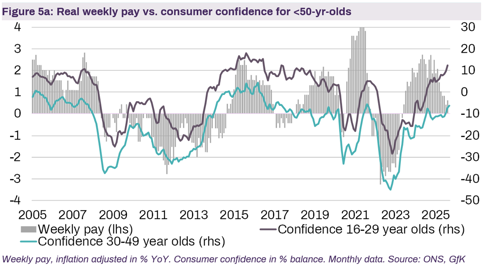

While it is normal for younger cohorts to be more optimistic than older cohorts, it is not normal for confidence among the young and old to move in opposite directions (Figures 5a and 5b). Since 2022, however, such a divergence has happened. In the past three years, younger cohorts — who own fewer assets, and hence are sensitive to wage trends — have grown more confident, thanks to healthy real income growth. In contrast, older, wealthier cohorts have lost confidence as real house prices have stagnated, and mortgage costs have risen.

Crowding out: the big squeeze on the private sector

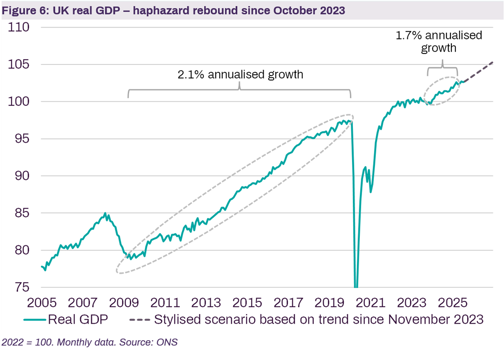

It is all-too-common to read analysis which describes the UK as a stagnating economy. This is wrong. The UK has managed annualised growth of 1.7% since late 2023 (see Figure 6), when the Russian gas supply shock started to ease, and shortly after the BoE ended its tightening cycle. Far from stagnation, this rate is probably close to the UK’s longer-run potential rate. But for the start of an upswing, and following major shocks – which are typically followed by a period of rapid catch-up growth, this is slow-going.

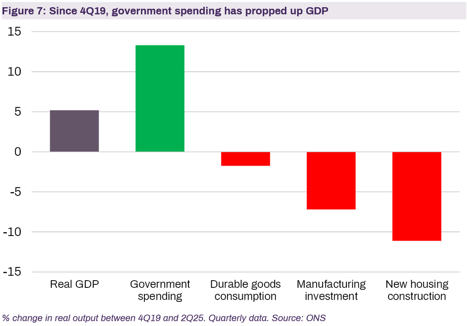

In my view, the story I have outlined so far is consistent with a crowding out effect – which is when overgrowth in government spending and too much borrowing hold back and even reduce private sector investment and consumption. The data in Figure 7 appear consistent with this diagnosis. Since 4Q19, real GDP has grown by 5.2%. And whereas government current spending has grown by 13.3% over the same period, durable goods consumption, manufacturing investment and new housing construction have declined by 1.8%, 7.2% and 11.2% respectively.

Crowding out harms economic performance in two ways. First, excess public borrowing pushes up benchmark interest rates to levels which are prohibitively high for a healthy expansion in activities that depend a lot on debt-financing – such as business investment, construction, and housing. Second, the excessive expansion of government spending takes scarce resources away from the private sector where they could be used to grow productivity, profits, and real incomes.

UK public spending has risen as a share of GDP from 39% in 2019 to around 45%, after peaking at over 50% during the pandemic. As often happens through shocks, a ratcheting effect occurred — spending rose sharply during the crisis, but did not fully unwind once the conditions that had justified it ceased.

To finance this massive rise in public spending, taxes as a share of GDP have leaped to a post-war high of 41%, from 36.5% in 2019. Despite the tax surge, government continues to face difficulties putting the public finances on a sustainable trajectory, and looks likely to try to increase taxes again.

The government needs to fix, not fiddle

While the choices Reeves makes at the 26 November budget can help partly mitigate the damage done, especially if she sets public finances on a sustainable course in a way that does not further spook markets by harming growth or pushing up inflation, it may not be enough to fully restore credibility.

So what options does the chancellor have?

One idea, rumoured before the election, could be to divide HM Treasury into two separate departments – perhaps with one semi-independent unit focused squarely on policies aimed at promoting long-term growth.

Another option, which could have a decisive impact, would be to reset fiscal policy in a way that prevents ballooning public sector debt as the population ages. In its March 2025 Economic and Fiscal Outlook, the OBR wrote:

“The long-term fiscal outlook remains very challenging, with pressures from an ageing population, climate change, and rising geopolitical tensions putting the public finances on an increasingly unsustainable path. The baseline projection in our 2024 Fiscal risks and sustainability report would require fiscal tightening of 1.5 per cent of GDP per decade over the next 50 years to return debt to pre-pandemic levels. Leaving policy settings unchanged in the long term would see debt rise to over 270 per cent of GDP by the mid-2070s.”

Setting out the precise steps to address this issue is far beyond the scope of this analysis. But raising taxes to fill the gap is not a sustainable solution. Current taxes are already a significant burden to growth. Raising them substantially further would be self-defeating. Instead, policymakers need to grasp the nettle and bring long-term spending under control. If that happened, global bond markets would anticipate a lower trajectory of gilt issuance relative to demand, immediately lowering benchmark rates across the curve and unlocking growth in the private sector.

Concluding remarks

The UK is not in a state of crisis, despite headlines suggesting so. Instead, it is in a state of subtle, but serious dysfunction. Policymaker credibility has eroded, leaving markets wary, and interest rates excessively high. Households, reeling from a sharp wealth shock, have retreated into saving, stifling consumption, and undermining recovery. Meanwhile, surging government spending crowds out private investment, and consumption.

The result is an economy that grows, but lacks the usual cyclical vigour that marks the start of an upswing. Momentum is sapped by fiscal uncertainty, elevated taxes, and the lingering effects of past policy missteps.

Restoring economic dynamism may require the kinds of bold innovation seen in the past, signalling a commitment to sound money, and a serious attempt to address long-term spending pressures. Until then, the UK risks remaining trapped in a slow-growth lane, where public sector expansion comes at the expense of private growth, and persistent caution prevails.