Following a publication break in April, where we took additional time to properly assess the impacts of recent market events, we publish our latest IPO Speedometer, a gauge on the health of the UK IPO market.

This month, the Speedometer has decelerated again, from 25mph to 22mph. The Speedometer remains in second gear, classifying the UK IPO market as ‘selectively open’.

This month, the broader market volatility following President Trump’s announced tariffs has dominated the IPO market backdrop. Volatility and uncertainty, both of which are heightened, create a more difficult immediate market environment for IPOs, pushing the Speedometer lower and making near-term IPO conditions more difficult.

IPO activity has remained European-led so far in 2025, with UK activity previously expected to pick up after Easter. The recent market volatility has caused many of these potential issuers to shift their timetables to post-summer, with certain issuers keeping optionality on later 2Q windows. The positive is that the UK IPO pipeline remains constructive.

Market volatility driving current IPO sentiment. IPOs tend to be a cyclical product, correlated to market conditions and volatility. This takes into account the roughly four-week live deal period, relatively low liquidity/free float post-IPO, and the importance of the immediate aftermarket. Although not a firm guideline, it is generally accepted that volatility, as measured by the VIX (US) and V2X (Europe), should be below 20% to be supportive for IPOs. Following recent events, they are currently trading at 25% and 21% (having spiked much higher), highlighting a challenging backdrop for immediate deals and moving the Speedometer lower.

Mixed IPO success in Europe and the US. IPO activity has been European-led so far this year, in addition to the US. There has been mixed success on European IPOs, with only three out of seven currently trading up on issue. They have either been larger, higher-quality issuers or those that are supported by strong domestic demand. US activity has also been mixed, with two notable offerings, CoreWeave and Venture Global, both disappointing, either by deal restructuring or by performing poorly in the aftermarket. This highlights the similar issues and sensitivities experienced by global IPO markets currently – deals need to be the right company (higher quality) and have the right transaction setup to be successful.

IPO timetables shifting to the right. We were previously expecting UK IPO activity to pick up after Easter once issuers confirmed FY24 results. The recent market volatility has caused many issuers to rethink near-term timetables, particularly those targeting 2Q transactions. With the rebound in market levels and improved sentiment in recent weeks, some are keeping optionality on later pre-summer windows, although most have shifted to post-summer. The post-summer timetables remain on course, although potential issuers and shareholders are monitoring conditions closely and hoping for a further improvement in the backdrop before launching. Recent market momentum has been encouraging.

Key drivers of the model this month

Broader market backdrop volatile, although some stabilisation in recent weeks

The principal driver of the IPO Speedometer and the overall market backdrop at present is the market volatility on the back of President Trump’s proposed tariffs. Following a constructive start to the year from the perspective of markets, with various global indices hitting all-time or recent-year highs, they traded off from mid-February, principally on the back of speculated, and then confirmed, US tariffs. US indices (S&P 500 and Nasdaq) hit correction territory in mid-March, falling more than 10% from their highs, and the Nasdaq entered a bear market in early April.

It is worth noting the meaningful rebound in market performance in recent weeks following the 90-day pause on tariffs excluding China. Market levels are now similar to those prior to Liberation Day. We have also noted a positive pick-up in investor sentiment on our sales desks. Although markets do feel better, uncertainty remains elevated around potential outcomes, and fund managers, particularly in the UK, remain constrained in their ability to put money to work quickly.

We continue to see the theme of UK and European outperformance play out. There is a good argument that, with the UK at the low end of tariffs, having a less export-led manufacturing economy than Europe, and being outside of the EU, there could be some relative benefits to the UK and its stock market. In addition, it comes from an attractive starting point with lower valuations. Investors are also now starting to question previous assumptions on the US around expected outperformance, pro-growth policy, and political stability. It was interesting to note the sell-off in the US dollar and treasuries (typical safe havens) recently, which highlighted the loss in confidence in the region.

In sum, markets are improving, and there are reasons to be relatively positive on the UK. However, significant uncertainty on outcomes remain. What this means is increased confidence in the near-term quick-to-market ECM pipeline, such as blocks, but most IPO issuers will be hoping for further stability before looking to launch their deals.

European IPO market generally on pause, for now

Following a fairly constructive start to the year, European IPO activity has slowed on the back of the increased market volatility, with a number of issuers pausing processes. Despite this, we have seen two small IPOs launch recently in Germany (Pfisterer) and Greece (Qualco).

The performance of European deals has been mixed so far this year, with only three out of seven IPOs trading up. There has been investor sensitivity on deals to valuation, deal structure (sizing, primary), and leverage. Another feature on deals, especially in the Nordics, has been cornerstone orders to de-risk transactions. We expect both anchor and cornerstone orders to continue as a theme in the current volatile backdrop to give confidence on deal execution.

The European deals that have been working well this year have been a mix of larger, high-quality, and liquid companies, and deals anchored by local demand (eg transactions in the Nordics, Türkiye, and Poland). Deals in between those two buckets have found it difficult.

UK IPO activity was previously expected to pick up after Easter, but has now generally shifted to the right. It was positive to see the £98m MHA (a British accountancy firm) IPO price and trade on AIM in April, and, separately, a small fund IPO (Achilles Investment) in February. They represented the first material UK IPOs (over £30m) since Applied Nutrition in October 2024. We do not see this as a function of a relatively weaker UK market, but rather a result of the supply of companies in the pipeline, with more higher-quality companies immediately ready to IPO in Europe.

US IPO market strained

The LSE has done a great job recently of bursting some of the myths around US IPOs, particularly for UK or international companies. We plan to follow up with a more detailed piece on our views, but we highlight that the US market is experiencing some of its own problems with performance at the moment, even with domestic issuers.

Two of the highlight IPOs in the US have been CoreWeave (a cloud platform for AI, $1.5bn IPO) and Venture Global (an LNG exporter, $1.75bn IPO). In order to price the transaction, CoreWeave restructured its transaction, pricing below its initial price range and reducing the deal size from $2.7bn to $1.5bn. Venture Global is currently trading at 65% below the IPO price.

A number of high-profile issuers have filed for potential US IPOs, such as Klarna and StubHub; however, these are rumoured in the press to have paused their IPO plans for now given the market volatility.

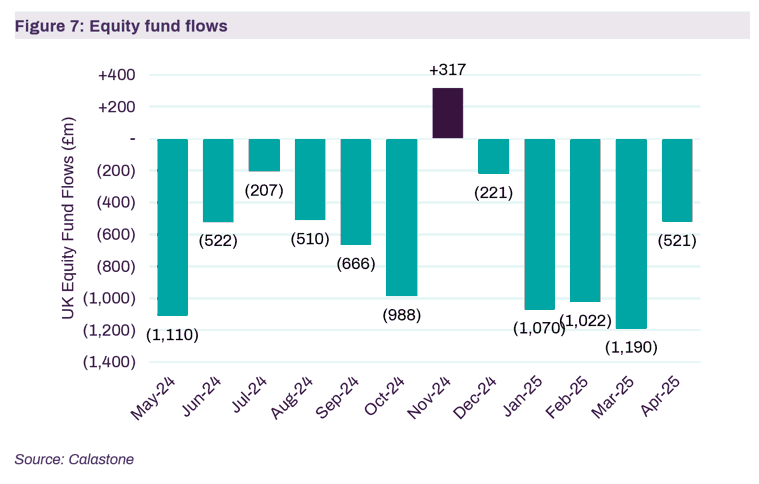

UK-focused equity funds see continued outflows

UK-focused equity funds saw outflows of £521m in April. Taking a positive spin on the data, it was one of the smaller outflows seen in recent months. The broader equity fund flow picture remains constructive, with inflows into both US and global equity funds despite the uncertainty around tariffs.

We have now seen almost four years of outflows from domestic UK equity funds, with outflows in 46 of the past 47 months. The recent change in tone in geographic preference for UK and Europe equities over the US has not yet translated into significant inflows, but we are confident that this will improve.

Commentary on other inputs this month

Frequency of M&A deals announced – The number of M&A deals and potential deals announced has remained steady over the past two months, with some high-profile companies under offer and continued high levels of speculation in the press on potential M&A deals.

Engagement from investors in pre-IPO meetings – We continue to see positive engagement from UK long-only funds, in particular on pre-IPO meeting processes, with high-quality meeting schedules and engagement. There is no doubt that investors want to see UK IPOs come to market and are expressing interest, even with the volatile backdrop.

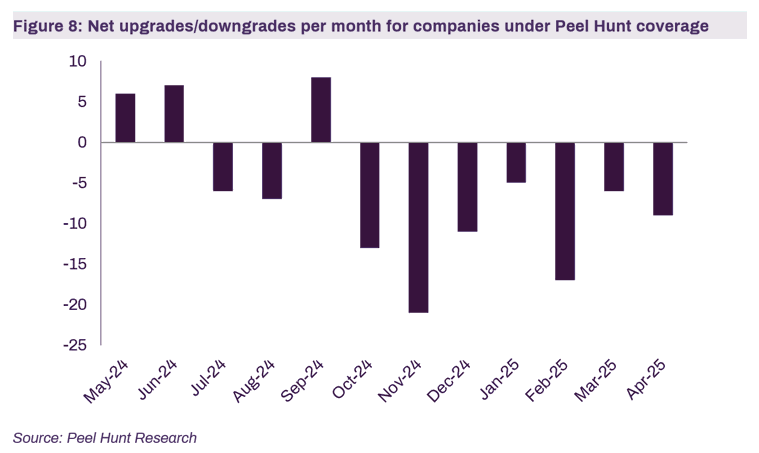

Earnings trend – 2025 YTD has continued the trend of net downgrades, marking eight consecutive months of net downgrades.

Potential UK IPOs

The companies listed below are rumoured in the press to be considering a UK IPO over the short to medium term (with many considering other exchanges too).

The pipeline is expected to show a broadening of activity, which was focussed on founder-led midcap issuers over the past 12 months, to more private equity and corporate-backed companies later this year; this will present its own challenges in a market that is still reopening.

There are a number of other themes emerging around the pipeline:

- A strong presence of financials and fintech companies

- A number of international companies looking at listing in the UK

- The corporate spin-off theme is prominent in both the potential European and UK IPO pipelines

- The international listing debate continues (UK vs US in particular), principally at the more jumbo end of issuers

Background to the PH IPO Speedometer

The IPO speedometer is a tool for potential issuers, shareholders and investors to accurately assess the current health and outlook of the UK IPO market. Based on a proprietary model with over 25 qualitative and quantitative inputs, it gives a numerical score (0-60mph) for the health of the UK IPO market. It is published on a bimonthly basis.

Methodology and inputs for the PH IPO Speedometer

In order to calculate the speed of the Peel Hunt IPO Speedometer in any month, we assess datapoints across eight main buckets, giving each bucket an overall score. These buckets are then split into primary and secondary drivers of the UK IPO market and a weighting (depending on their importance) is assigned to each overall score. This then provides us with the output in the 0-60mph range. The eight main buckets and their inputs include the following:

- Equity fund flows (primary driver)

- Volume and performance of IPO/ECM activity (primary driver)

- General investor sentiment (primary driver)

- LO investor engagement (primary driver)

- Market stakeholder objectives/expectations

- Equity market performance

- Macro backdrop

- Broader trading activity/market liquidity