· This month, the Speedometer has decelerated slightly to 25mph. The Speedometer remains in second gear, classifying the UK IPO market as “selectively open” for either best-in-class issuers or certain niche thematics that resonate.

· The key drivers of the model this month were: a European-led IPO reopening in 2025 with limited UK activity so far, a positive start to broader UK ECM, UK macro rebounding from concerns at the start of the year, and global equity markets pushing against all-time highs again. Following a brief reversal in November, UK domestic equity fund outflows resumed in December and January.

· With a lack of UK IPO issuance so far this year, the Speedometer has decelerated slightly. We still see the backdrop as constructive for IPOs but sustained inflows and more IPO activity will be needed for the market to fully open.

We have been expecting 1Q25 to be quiet for UK IPOs for some time and this has proven to be the case. 2024 showed positive, although gradual, progress in the IPO market and we expect this to continue into 2025, albeit from 2Q onwards. We still see the market as selectively open for the right issuers.

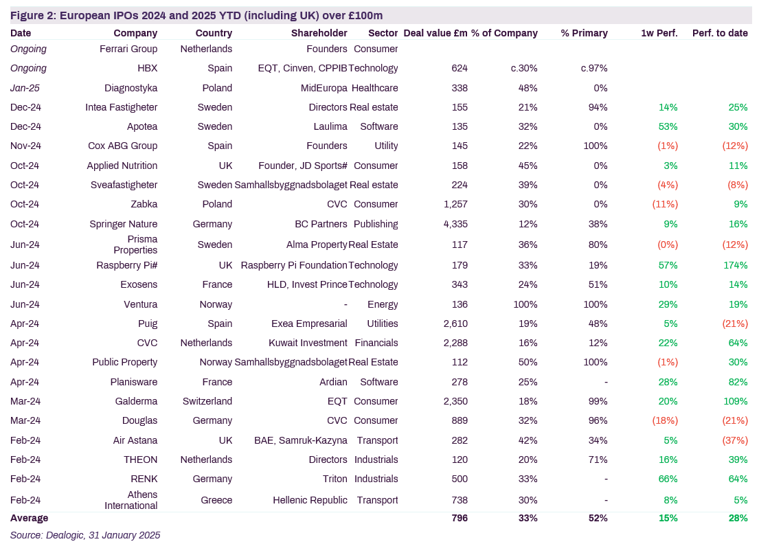

European-led IPO reopening so far in 2025. IPO activity has restarted in Europe with three notable offerings currently live in the market (Dutch luxury travel logistics firm Ferrari Group, Spanish travel technology company HBX Group, and Czech power equipment company Doosan Skoda Power), and Polish medical diagnostics firm Diagnostyka priced its IPO last week. We are yet to see IPO activity resume in the UK. However, we have been expecting 1Q to be quiet for some time, with most pipeline issuers targeting 2Q, on the back of their FY24 results, at the earliest.

Broader conditions remain positive. Equity markets in the UK and globally have bounced back from bond yield concerns earlier in the year and are trading at near highs again. Whilst we entered the year with a relatively constructive outlook for the UK, particularly compared with Europe, that sentiment was tested with rising yields. We appear to be back on a steadier footing now, but risks clearly remain to the outlook. Broader UK ECM has started the year well with c.£4bn of issuance so far. Demand is clearly there for the right situations.

UK IPO activity expected to ramp-up in 2Q. A number of issuers are currently monitoring windows in 2Q, which we expect to be the first real test of the UK IPO market in 2025. We expect the pipeline to show a broadening of activity, which was focused on founder-led mid cap issuers in 2024, to more private equity and corporate backed companies in 2025.

Key drivers of the model this month

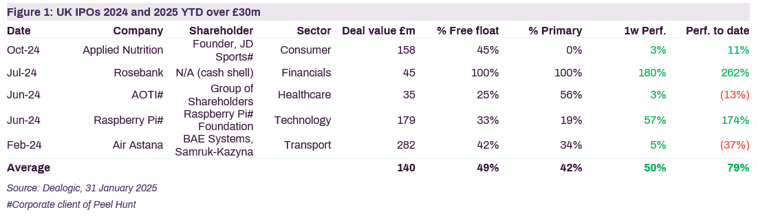

IPO activity re-opens in Europe but limited in UK so far in 2025 YTD

European IPO activity has re-opened with two notable offerings currently live in the market with deal values greater than £100m: Dutch luxury logistics company Ferrari Group and Spanish travel technology company HBX Group. Furthermore, Polish medical diagnostics firm Diagnostyka priced its IPO last week and is due to start trading on 7 February. We expect these deals to make up the bulk of the near-term European pipeline, with most issuers looking to launch post their FY24 results, either at the back-end of 1Q or post Easter.

IPO activity has remained muted in the UK, as we expected, with the near-term pipeline targeting launches from 2Q onwards. With Easter falling in mid-April this year, the pre-Easter window represents a tight one, with more flexibility post Easter. This continues the theme that we saw throughout 2024 of it principally being a European-led IPO recovery.

Positive start to broader UK ECM activity in 2025

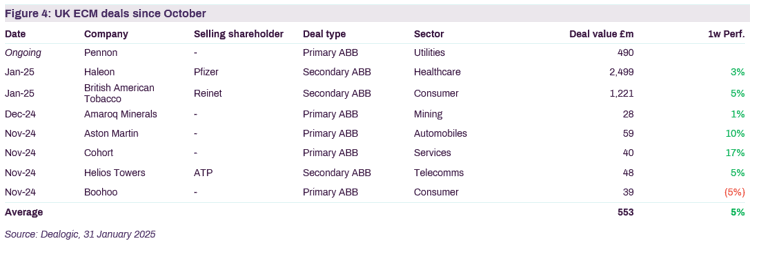

Broader UK ECM saw a constructive start to 2025, with two jumbo block selldowns in Haleon by Pfizer (£2.5bn) and in BAT by Reinet (£1.2bn). Both of these selldowns performed well in the aftermarket, trading up 3% and 5%, respectively.

This continues the theme in 2025 of elevated overall ECM volumes in the UK compared with other European exchanges (see Figure 5). Although it has been a European-led IPO recovery, the broader ECM picture remains constructive in the UK.

UK equity and macro outlook back on relatively positive terms

Going into 2025, there was a sense of optimism around the UK macro and equity outlook, particularly relative to Europe. If you take some of the key themes expected to shape markets this year (e.g. trade tariffs, deregulation, pro-energy policies), you would expect the UK to compare favourably with Europe given its higher weighting of sectors expected to benefit (i.e. more banks and energy, less export-driven or manufacturing industries). UK GDP growth, although not spectacular (UK consensus 1.4% in 2025), was towards the top of estimates for the G7 (stripping out North America).

However, spiking bond yields at the start of the year softened sentiment somewhat. Although much of this was driven by global concerns around potential higher inflation and central bank rates, there was an outsized impact on the UK, which highlights some of the credibility issues on the region. Our view at Peel Hunt was that the UK moves were mostly overdone and would likely self-correct, which has turned out to be the case. This was helped by some positive UK and global macro prints and various positive headlines on the UK (e.g. around deregulation and investment). Short-term concerns here seem to have fallen away but it is a reminder that various risks remain around the outlook for this year.

Global equity markets back near highs and volatility remains subdued

Global equity markets shook off concerns around spiking global bond yields earlier in the year and have moved back towards record highs (S&P 500 hit a record high in late January), post Trump inauguration optimism and a strong tech run, notwithstanding concerns about the impact of global tariffs.

Volatility also remains at supportive levels for IPO issuance, with the VIX (US volatility) at 13% and the V2X (European volatility) also at 13% at 31 January, within the common perceived supportive level of 20%.

UK-focused equity funds see resumption of outflows

Despite November seeing the first UK-focused equity fund inflows in 42 months, with inflows of £317m, outflows resumed in December and January (source: Calastone, Figure 8). December’s net selling of £221m was the ‘least bad outflow’ since May 2021. However, in January, UK-focused funds were hit with £1.07bn of outflows, the sixth-worst month on record.

The broader equity fund flow picture was mixed with European and Asia-Pacific funds seeing outflows, while North American equities saw inflows of £576m.

Commentary on other inputs this month

- Frequency of M&A deals announced – The number of potential deals announced has remained low over the past two months, consistent with the level seen in 2H24. There are still high levels of speculation in the press on potential M&A deals.

- Engagement from investors in pre-IPO meetings – We continue to see positive engagement from UK long-only funds in particular on pre-IPO meeting processes, with high quality meeting schedules and engagement. Where there are compelling opportunities, investors are putting their hands up to participate. With a number of UK IPOs now targeting 2Q, the upcoming deep dive and pilot fishing exercises will be an important test of whether there is firm demand from investors for these transactions.

- Earnings trend – December and January continued the trend of net downgrades, marking four consecutive months of net downgrades.

Potential UK IPOs

There is speculation in the press that the following companies are considering a UK IPO over the short-to-medium term (with many considering other exchanges too).

The pipeline is expected to show a broadening of activity, which was focused on founder-led mid cap issuers in 2024, to more private equity and corporate-backed companies in 2025 – that will represent its own challenges in a market that is still re-opening.

Several other themes are emerging around the pipeline:

- Strong presence of financials and fintech companies.

- The number of international companies looking at listing in the UK.

- Corporate spin-off theme prominent in both the potential European and UK IPO pipelines.

- International listing debate continuing (the UK vs the US in particular), principally at the more jumbo end of issuers.

Background to the PH IPO Speedometer

The IPO speedometer is a tool for potential issuers, shareholders and investors to accurately assess the current health and outlook of the UK IPO market. Based on a proprietary model with over 25 qualitative and quantitative inputs, it gives a numerical score (0-60mph) for the health of the UK IPO market. It is published on a bi-monthly basis.

Methodology and inputs for the PH IPO Speedometer

In order to calculate the speed of the Peel Hunt IPO Speedometer in any month, we assess datapoints across eight main buckets, giving each bucket an overall score. These buckets are then split into primary and secondary drivers of the UK IPO market and a weighting (depending on their importance) is assigned to each overall score. This then provides us with the output in the 0-60mph range. The eight main buckets and their inputs include the following:

- Equity fund flows (primary driver).

- Volume and performance of IPO/ECM activity (primary driver).

- General investor sentiment (primary driver).

- LO investor engagement (primary driver).

- Market stakeholder objectives / expectations.

- Equity market performance.

- Macro backdrop.

- Broader trading activity/market liquidity.