This month the Speedometer has deaccelerated slightly to 27mph, down from 29mph in August. The Speedometer remains in second gear, classifying the UK IPO market as “selectively open” for certain issuers.

The key drivers of the model this month were: IPO activity reducing post summer in both the UK and Europe, continued constructive broader UK ECM volumes, a resilient equity market backdrop, and continued outflows from UK domestic funds.

Movement in the IPO Speedometer has principally been driven by the lack of supply of immediate IPO-ready issuers, rather than weakening market fundamentals.

We continue to classify the UK IPO market as ‘selectively open’ for either best-in-class issuers or certain niche thematics that resonate. We expect some limited IPO transactions in the UK over the remainder of the year and do not expect a broader re-opening until 2Q25.

IPO activity has reduced post summer. 1H saw the resumption of IPO activity in both the UK and Europe, with the UK activity more back-end weighted in that period. After this momentum earlier in the year, the post summer window has been less active than was previously hoped in both the UK and Europe. This has been driven by the lack of supply of immediate IPO-ready issuers and a wish to avoid potential volatile windows around the UK budget and US election, rather than a weakening in market fundamentals or investor support.

Backdrop remains supportive for select issuers. There are a number of factors that give us confidence that the IPO market remains open for the right issuers. We have seen the continued positive performance of IPOs that have priced in the UK and Europe, significant broader UK ECM issuance across product types and market cap ranges, and a clear willingness from investors to participate in deals. Headline fund flows remained negative, but investors have money to put to work for the right deals.

Broader re-opening expected in 2025. Despite the lower IPO volumes post summer, there are a number of UK issuers either doing early-stage investor meetings or commencing the preparation to get ready for an IPO in 2025. Where we have run early look processes at Peel Hunt, there has been a positive reaction from investors who want to see deals come to market, assuming they are quality issuers, pursuing a reasonable deal size, and at the right valuation. We are expecting a select number of IPOs to price in the UK over the coming months and a broader re-opening in 2Q25.

Key drivers of the model this month

UK and European IPO activity subsides post summer

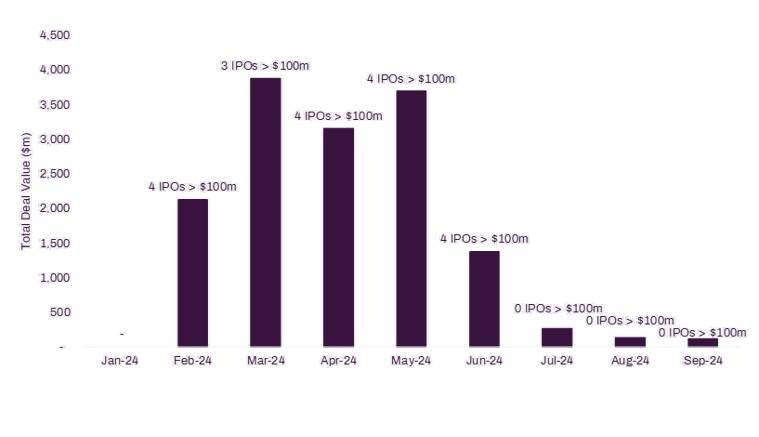

Having seen a general broad resumption of IPO activity across Europe in 1H, activity has slowed over recent months and has continued to do so post summer (Figure 1). Although UK IPO activity was more 2Q-weighted, that too has slowed post summer.

The UK saw its first post summer IPO, supplement maker Applied Nutrition, launch in recent weeks. The deal is currently in PDIE (i.e, analysts educating the market) and is expected to price over the coming weeks. This compares with the three IPOs we saw price in the UK over June and July (Rosebank, AOTI# and Raspberry Pi#). The UK activity and pipeline still has a very mid-cap focus to it, compared with some of the more jumbo activity seen in continental Europe.

In Europe, three principal deals have been launched post summer: academic publisher Springer Nature in Germany; retailer Zabka Polska in Poland; and frozen baked goods company Europastry in Spain (subsequently pulled). This does represent a continuation of the re-opening of the market in Europe but is a smaller group of deals than was hoped for a couple of months ago, following some of the flagship deals earlier in the year.

There are two main drivers of this reduction of activity in both the UK and Europe. Firstly, it is a function of where companies are in their preparation to list. Many companies are taking confidence from the resumption of IPO activity earlier in the year but are targeting 2025 listings given the preparation lead time required. Secondly, particularly in Europe, issuers are avoiding a potential volatile upcoming window with US elections in early November. In the UK, we are expecting issuers in ECM generally to avoid the immediate window around the UK budget on 30 October.

European IPO issuance YTD is £14bn, up 69% on the same period in 2023. Overall, it is a product that is working well, with average one-week aftermarket share price performance of 18% (Figure 3). The first notable IPO post summer was academic publisher Springer Nature who listed in Germany and traded up 8% on day one, continuing that trend of positive performance. Although the deal count has reduced, IPOs continue to work well for the right companies with the right deal set up.

Figure 1: IPO activity decreasing – European IPOs (including UK) 2024 YTD

Source: Dealogic, 01 October 2024

UK ECM activity continues to broaden with mixed success post summer

Post summer, UK ECM activity has remained active, with a particular focus on secondary selldowns. Following the recent resilient equity market performance and with potential upcoming volatility from the UK budget and US elections, issuers and shareholders have targeted windows in recent weeks to get deals done.

Similar to the IPO market, the activity was initially more mid-cap in focus, but recently we have seen a flurry of activity with larger offerings for Haleon (secondary selldown, £2.4bn) and British Land (£293m, primary raise), also highlighting the broad range of offerings we are currently seeing in UK ECM across market caps, products (IPO, primary raises and secondary selldowns) and sectors.

It is worth noting that the performance of some of these blocks has been mixed, with a number trading below issue post pricing. We see this underperformance as very deal specific, rather than any softening of the appetite for ECM overall.

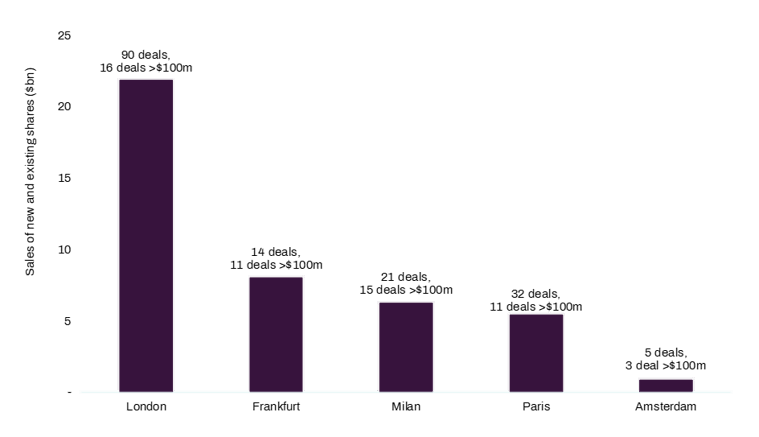

Overall, UK ECM issuance (ex-IPOs) continues to be well-ahead of other European regions (Figure 5), with almost US$22bn of issuance YTD in the UK, c.3x the next highest region (Germany) and +32% vs the comparative period last year.

Figure 5: Sale of new and existing shares ex-IPOs 2024 YTD

Source: Dealogic, 01 October 2024. Only deals with deal value > $5m

Supportive equity market backdrop continues

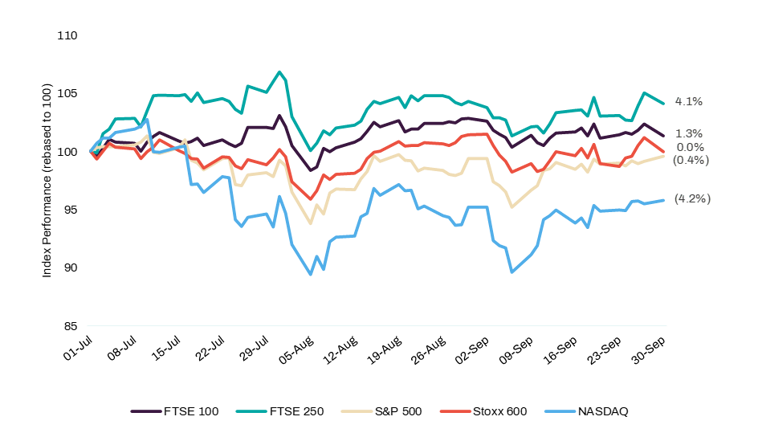

Following some short periods of volatility in August and September on the back of macro and geopolitical concerns, equity market indices have shown resilience and are again trading near highs (Figure 6). This was driven by continued central bank cutting (and the Fed’s 50bps cut in particular) and generally supportive macro data. Importantly for IPOs, volatility also remains at supportive levels (i.e, V2X and VIX both below 20).

Figure 6: Index performance since July 2024

Source: Refinitiv Workspace, 01 October 2024

UK domestic outflow picture remains strained

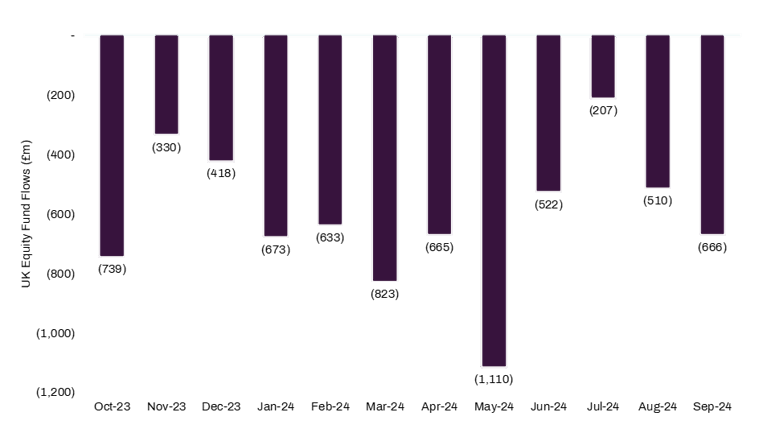

Headline outflows from UK domestic equity funds continue to persist, with the ominous September figure of £666m representing the 40th straight month of outflows (source: Calastone, Figure 7).

Although the headline number is negative, we are seeing investors putting money to work for the right deals. What it does not represent is the cash inflow certain investors see from buybacks and takeovers, as well as the bid from international funds.

The tone with UK investors had become more positive in recent months. However, we have seen a softening recently with some concern as we approach the UK Budget on 30 October, particularly around tax rates and what it might mean for corporates and also the capital markets (i.e, CGT and IHT). It is worth noting that this is more pronounced at the small/mid cap end of the market, rather than larger cap investors.

Figure 7: UK equity fund flows

Source: Calastone

Commentary on other inputs this month

- Continued strong relative overall fundamentals of the UK – As mentioned in our previous IPO Speedometer report in August, we are generally seeing increased investor confidence around the UK, helped by an improving relative political and macro picture. Although the tone has softened ahead of the UK Budget on 30 October, the UK is still seen as a relative bright spot in many respects.

- Frequency of M&A deals announced – The number of potential deals announced has remained low over the past two months, consistent with the level seen earlier in the summer. However, it is notable that the average equity value of UK takeovers in 3Q was six times higher than the level in 3Q23. There are still high levels of speculation in the press on potential M&A deals.

- Engagement from investors in pre-IPO meetings – We continue to see positive engagement from UK long only funds in particular on pre-IPO meeting processes, with high quality meeting schedules and engagement. Where there are compelling opportunities, investors are putting their hands up to participate. We would note that there is an increased number of these processes ongoing across the market in the UK (>10), with a broad range of assets, and it remains to be seen how many of these will successfully IPO.

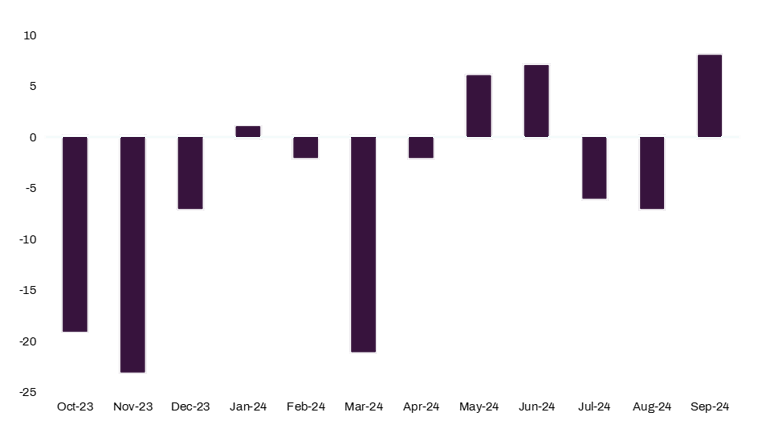

- Improving earnings trend – September saw a marked improvement in company updates compared to the negative earnings bias seen in July and August.

Figure 8: Net upgrades/(downgrades) per month for companies under Peel Hunt coverage

Source: Peel Hunt Research

Potential UK IPOs

The following companies are rumoured in the press to be considering a UK IPO over the short-to-medium term (with many considering other exchanges too).

A number of themes are emerging around the pipeline:

- Strong presence of financials and fintech companies.

- A number of international companies looking at listing in the UK.

- Corporate spin-off theme prominent in both the potential European and UK IPO pipelines.

- International listing debate continuing (UK vs US in particular), principally at the more jumbo end of issuers.

Background to the PH IPO Speedometer

The IPO speedometer is a tool for potential issuers, shareholders and investors to accurately assess the current health and outlook of the UK IPO market. Based on a proprietary model with over 30 qualitative and quantitative inputs, it gives a numerical score (0-60mph) for the health of the UK IPO market. It is published on a bi-monthly basis.

PH IPO Speedometer scale

Methodology and inputs for the PH IPO Speedometer

In order to calculate the speed of the Peel Hunt IPO Speedometer in any month, we assess datapoints across eight main buckets, giving each bucket an overall score. These buckets are then split into primary and secondary drivers of the UK IPO market and a weighting (depending on their importance) is assigned to each overall score. This then provides us with the output in the 0-60mph range. The eight main buckets and their inputs include the following:

- Equity fund flows (primary driver).

- Volume and performance of IPO/ECM activity (primary driver).

- General investor sentiment (primary driver).

- LO investor engagement (primary driver).

- Market stakeholder objectives/expectations.

- Equity market performance.

- Macro backdrop.

- Broader trading activity/market liquidity.