8 May 2026

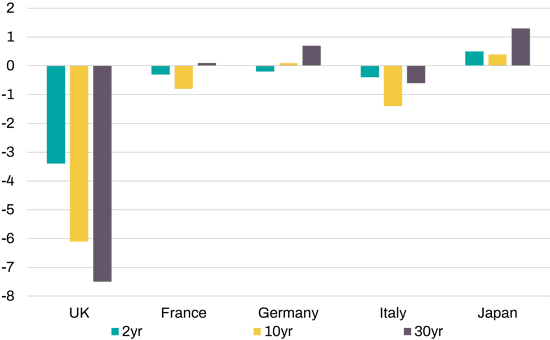

Initial market reaction to UK election results - change in bond yields

Change since the open on 8 May 2026 in basis points. Data as of 11:00AM GMT. US data excluded as markets not open at the time the date were taken. Source: Bloomberg

As the results from the English local elections roll in, a clear picture is emerging. Right-wing Reform UK, led by Nigel Farage, is surging – with sweeping gains in former Labour (centre-left) strongholds, while also taking support from the centre-right Conservatives. The centre-left Liberal Democrats and far-left Greens are both posting modest gains – but support for the Greens may be somewhat lower than their campaign and opinion polling momentum had indicated.

The results are a negative verdict on Prime Minister Keir Starmer's government and reflect predictable voter frustration over the economy, immigration, and taxes. The question of whether Prime Minister Keir Starmer can survive much longer now looms even larger than before – highlighting the risk of even near-term political uncertainty in case he faces a challenge to his leadership.

Yesterday, we discussed these issues in detail – considering potential contenders to replace Starmer and the process for doing so. Over the weekend, as more results come in and, probably, frustration among grassroots Labour Party members grows, we need to pay close attention for signs that any of his potential rivals may begin to position themselves for a challenge.

What strikes me most today, however, is the initial judgement of financial markets. As our chart of the week shows, UK gilt yields enjoyed an outsized decline this morning – versus broadly unchanged rates in other key markets which had also been open as the UK election news unfolded.

In the run-up to the vote, the risk to watch had been that bond yields could spike on fears that bad results for Labour could result in Starmer's sudden collapse combined with lurch to the left by Labour following a leadership contest. The initial (positive) reaction by gilt markets therefore appears counterintuitive.

At this stage, we can only make our best guesses. But I suspect there are three drivers:

- Starmer has signalled a willingness to fight on, while no challengers have come forward yet.

- Support for the Greens has been modest, against huge support for Reform. If the tide of public opinion is shifting towards right-wing parties in favour of deregulation, scrapping anti-growth green energy policies, and lowering taxes and public spending, Labour would not be doing itself any favours by swapping out Starmer for a candidate who is further to the left.

- Markets may be looking ahead to the next general election (due in August 2029 at the latest) and reasoning that the UK is tilting in a more market-oriented direction – which may explain the steeper decline in yields at longer maturities as worries over the longer run direction of the economy ease at the margin.

At any rate, it is far too early to draw any strong conclusions and the situation is in flux. As ever, therefore, please take my knee-jerk reactions such as these with a healthy dose of salt.