7 May 2026

The narrative for the UK economy has deteriorated materially over the past couple of months. At the start of the year, disinflation and falling interest rates looked set to support a gradual recovery in momentum, allowing struggling Labour Prime Minister (PM) Keir Starmer and Chancellor Rachel Reeves to navigate a predictably difficult summer after likely heavy losses in today’s local elections in England and the national parliamentary elections in Scotland and Wales. The Iran war and the closure of the Strait of Hormuz have upended that outlook, unleashing a global energy and supply shock that risks trampling green shoots of growth while reigniting inflation. Money markets have abandoned erstwhile bets on two further Bank of England (BoE) rate cuts this year, in favour of two to three hikes.

Under Starmer and Reeves, Labour had campaigned and won the 2024 general election on easing cost-of-living pressures and restoring growth. After two years of choppy expansion, outsized inflation, and Starmer’s mishandling of the Mandelson–Epstein scandal, the Iran shock will intensify pressure on household budgets and raises genuine questions about how much longer the pair can survive. If voters deliver heavy losses to Labour today by switching to the far-left Greens or right-wing Reform, the key risk is that the party concludes ‘enough is enough’ and moves against Starmer. If that occurs, the danger of a sharp leftward lurch by the government looms large.

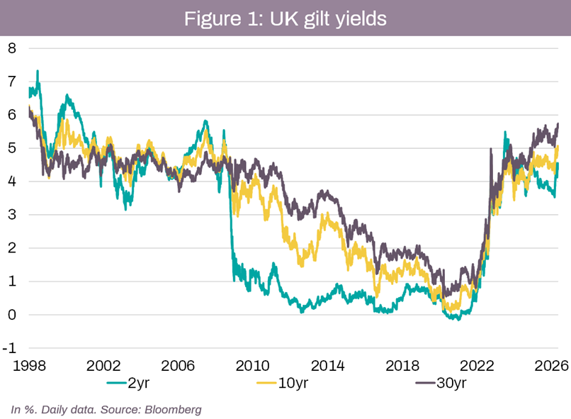

Against this backdrop, it is no surprise that the ever-sensitive gilt market has come under renewed selling pressure, with the 30-year yield hitting its highest level since 1998 (Figure 1). Of course, how this story unfolds is anyone’s guess. Still, I find the balance of risks tilted towards the economic and political situation improving on a six-month horizon rather than worsening. Let me make some observations that hopefully add some colour and nuance:

- Iran and local election risks are interacting in a way that reinforces growth and inflation worries, while bond markets are being asked to contemplate a worst-case scenario of a protracted conflict and lasting global supply shocks, plus risks associated with a Labour leadership election. While the worst-case scenario is probably not yet fully priced into gilts, because that is the direction in which market pricing is skewing, a sharp positive re-rating looks likely if one or both these risks do not play out.

- The UK is an inflation outlier, not a debt outlier. Ordinary measures of fiscal health, such as current annual borrowing as a percentage of GDP or its medium-term direction, as well as the debt-to-GDP ratio, do not explain the UK’s outsized borrowing costs. For instance, whereas the UK has the highest borrowing costs in the G7, it ranks in the upper half of the table for its overall fiscal position. However, over the past 10 years, the UK has suffered the most inflation in the G7. In my view, this (inflation) is the source of the market’s concern. Put differently, with inflation under control, but with the same fiscal outlook, I suspect UK borrowing costs would, by now, have fallen back towards their historical trend somewhere in the middle of the G7 pack.

- The UK was on a disinflationary trend prior to the war and gilt markets had been rallying. While an unravelling of the Starmer government could put further upward pressure on yields – especially if Labour seriously contemplates a lurch towards a more interventionist policy stance – the UK bond market rallied strongly yesterday on rising hopes of a deal to end the Iran war and reopen the Strait of Hormuz. On the eve of the war, the 10-year gilt yield was 4.2%. In late April, when worries of a protracted Iran war jumped, the 10-year rate hit 5.1%. At the time of writing, the 10-year yield is trading at 4.9% – 20bps lower than peak as hopes that the Iran war can end soon have edged up.

- An end to the war and the re-opening of the strait would likely drive yields significantly lower as inflation risks faded and markets further curtailed bets for rate hikes – even if UK domestic political risks remained. In our view, the BoE will be able to avoid rate hikes if the war is ended. If markets fully priced out BoE hikes, that alone could take out another 40-50bps from the 10-year rate.

- Elevated gilt yields engender fears that a policy mistake could trigger another Truss moment – they are thus a gift to Starmer and Reeves and act as a check and balance against a lurch towards anti-growth or inflation policies in case of new Labour leadership. Whichever duo wishes to try replacing Starmer and Reeves will need to put forward a coherent plan for growth and fiscal sustainability that also does not increase inflation pressures. As it stands, none of the likely candidates for leadership offer any serious alternatives. Possible contenders (see next section) such as Manchester Mayor Andy Burnham have only agitated fears with their hints at nationalising parts of industry or claims that the UK should not be ‘in hock’ to bond markets.

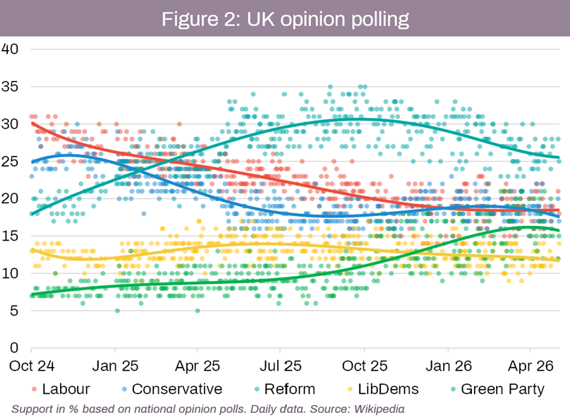

- Big swings in English local elections towards the Greens and Reform may not be a good indicator of voting patterns at the next general election (due before August 2029). A lot will depend on how voters perceive their performance in running any councils in which they gain control. Campaigning and winning support with eye-catching promises is a different beast from the harsh, and often mundane, reality of running councils on tight budgets in a way that already dissatisfied locals find acceptable. If Reform and the Greens struggle to govern at the local level, it will put people off voting for these parties in the next general election. In last year’s May local elections, Reform won the highest share of the popular vote (30%) and, shortly after, their support in national opinion polls peaked at around 32% (Figure 2). Since then, their support has slid to just 25%. While a number of factors may be behind this, including Reform leader Nigel Farage’s initial support for the US’s war on Iran – a war that is unpopular with the British public – reports suggesting Reform has underperformed expectations in their running of local councils may be part of the story too.

- If Labour changes leader, a general election does not automatically follow. Because Labour holds a majority in the House of Commons, the party’s internal rules are sufficient to decide who would be the next PM. Only a no-confidence defeat forces an election. While opposition parties may demand one, Labour could easily block it. Labour’s majority would keep any new leader in power unless (or until) divisions grow (allowing a no-confidence vote to pass) or a crisis unfolds that forces the new PM to go to the electorate for a mandate. If the government dramatically changed its policy agenda under a new leader (most likely in the case of Rayner), public pressure for a general election to seek a mandate would grow.

Top four challengers to Starmer, according to betting markets

- Angela Rayner: Former deputy leader who is supported by grassroots party members. Rayner remains under investigation by HMRC over her tax affairs. While this hurts her chances – and risks the narrative of replacing one scandalised PM with another – her popularity within the party suggests she may be able to consolidate the left with the moderates. Rayner, a trade unionist, would likely favour increased government spending and taxes on wealth, as well as further expanding workers’ rights.

- Andy Burnham: Manchester mayor, who, in January, was blocked from contesting a Westminster seat by Starmer. He is popular among the grassroots and has succeeded as Manchester mayor. He polls strongly but needs an MP seat, which would need to be coordinated by his supporters within the Labour Party before he could run. Whether his successful regional economic policies translate into successful national policies is an open question – his past snipes at financial markets and the UK’s creditors have alarmed investors.

- Wes Streeting: Health Secretary, economic centrist, but also a friend of Mandelson. His team has tried to distance him from the Mandelson scandal, but it may still hurt his chances. He draws moderate backing but faces opposition from the left wing of the party. Unions are critical of his centrist ‘Blairite’ views. His health policies have focused on improving services and productivity and may be an indication of his broader economic leanings. For markets, he would be viewed as a safer pair of hands than Rayner.

- Ed Miliband: Energy Secretary, left-aligned. Miliband is viewed as competent and experienced by party members who value his green leanings. He led the party from 2010–15 but failed to win a general election in 2015. Miliband would likely favour increased public spending, higher taxes, and a slower pace of deficit reduction.

What is the process for Labour electing a new leader?

- A challenger (a Commons MP) must secure written nominations from at least 20% of the Parliamentary Labour Party (PLP), currently around 81 of 403 MPs, which are submitted to the General Secretary. This initiates the process for a contest in which the incumbent (Starmer) is automatically included on the ballot without needing nominations. Of course, if Starmer were to resign, then a leadership election would automatically be triggered. In that scenario, Starmer would likely stay in post until a new leader is elected.

- The challenger must also obtain support from either 5% of Constituency Labour Parties (CLPs) or at least three affiliated organisations (including two trade unions) representing 5% of affiliated membership.

- Labour’s National Executive Committee (NEC) sets the election timetable. Qualified candidates then campaign via hustings, debates, and equal access to member data for communications. This process typically lasts weeks.

- Eligible voters – party members (with six months’ membership), affiliated supporters, and registered supporters – vote online or by post. They rank preferences until a candidate exceeds 50% of support.

- The winner is announced at party conference or a special event; if the challenger wins, Starmer resigns as leader and PM.