1 May 2026

Financial markets saw yesterday’s Bank of England (BoE) meeting as slightly dovish, cutting year-end rate hike bets from 3 to 2.6, while reducing the probability of a hike at the next meeting in June from 70% to around 60%. While the BoE warned that it may need to lean against inflation pressures with rate hikes if the war in Iran persists, it also highlighted the significant downside risks to growth arising from the related supply shocks.

The 8-1 vote split in favour of holding the Bank Rate at 3.75%, with BoE chief economist Huw Pill the lone dissenter in favour of a hike, was in line with our and market expectations. The BoE also kept its neutral forward guidance unchanged from March.

In our view, which is contingent on a normalisation of shipping through the Strait of Hormuz within weeks, the BoE will likely stay on hold over the summer while warning of potential rate hikes to help prevent inflation expectations from rising too much, before starting to ease again in Q4. However, the bar for a cut over the summer is falling as the disruption from the war worsens.

Given the uncertainties facing the UK economy and the complex policy trade-offs facing policymakers, the BoE did well with its messaging yesterday—striking a balance between warning of the inflation risks ahead, without overreacting with a knee-jerk policy tightening.

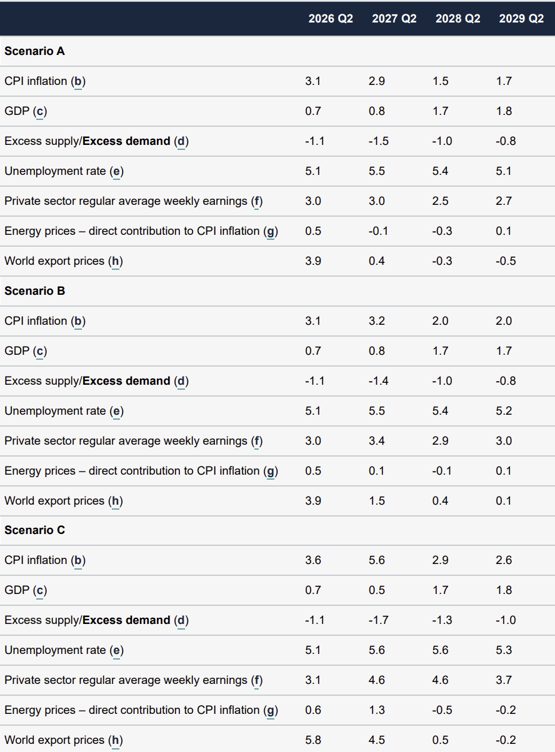

However, one area in which the BoE can still improve its guidance is its forecasts. In this meeting, the BoE provided three scenarios for how the economy may evolve—which are set out in the table above.

Besides the needless confusion arising from having to communicate how policy may react in three potential outlooks rather than one, I found the choice of scenarios somewhat at odds with underlying economic fundamentals. All three scenarios skew heavily towards potential inflation risks, with insufficient concern over the very real recession risks.

After all, this is among the biggest global energy supply shocks in history—and there is little evidence of strong demand in the UK to support skewing all alternative scenarios in a more inflationary direction - as the BoE has done with scenarios B and C.

In my view, a plausible downside outcome is scenario B for inflation in 2026 and 2027, but instead with a notable fall in output and a rise in unemployment—which would push inflation well below target from 2028 onwards and hence undermine the case for hikes.

Earlier this week, we set out in detailed analysis our 'cautious case against BoE rate hikes', in which we argue why the Iran shock is not like the Russia shock and why rate hikes are not necessarily the right medicine.